Assessment and outlook 17 years after market opening

MBA. Hellen Ruiz Hidalgo

Strategic Communicator

Foreign Trade Observatory (OCEX)

Vice-Rectory for Research - Distance Learning State University (UNED)

Historical context. After the civil war of 1948 and under the leadership of the National Liberation Party and the emblematic figure of José Figueres, Costa Rica adopted, starting in 1950, the public policy of Import Substitution Industrialization (ISI). This orientation assigned the State a decisive role in production, financial institutions, and the allocation of investments. The mechanism chosen to achieve these goals was the nationalization of large industrial conglomerates, such as the Costa Rican Electricity Institute (ICE), telecoms, the National Liquor Factory (FANAL), etc. In the field of public finance, banking and insurance also became state monopolies. In this way, the Costa Rican model had succeeded in placing the State in control of the main reins of the national economy. Until the mid-1980s, the system had functioned successfully, both socially and productively. Costa Rica had thus achieved the most advanced education system in Latin America, reputed to be 15 years ahead of the average for other Latin American countries.

The middle class experienced spectacular growth, and those years are generally regarded as the “golden age” of national development. In all social indicators, Costa Rica outperformed its neighbors. Those years are generally regarded as the “golden age” of national development. Costa Rica outperformed its neighbors in all social indicators. The political consequences that accompanied this progress were also remarkable, reflected in a highly functional democratic system, alternative forms of government, social cohesion, and high citizen regard for its institutions.

In the mid-1970s, however, Costa Rica fell into a serious international public debt crisis. In 1979, it declared default, but eventually had to resort to the assistance of the International Monetary Fund (IMF), under the ideological hegemony of a neoliberalism that advocated what was called the “Washington Consensus,” consisting, among other things, of improving public finances by reducing social investment, economic openness, and privatization of state entities related to production, trade, and finance. Costa Rica had to submit. However, the population appreciated its state-owned companies, especially ICE, which had brought electricity to remote areas where private companies would not have considered it profitable, FANAL, which supplied public hospitals with alcohol at subsidized prices, and the National Insurance Institute (INS), which also financed the Fire Department. It was this social support that gave strength to the political class to resist the breakup of these monopolies and the privatization of these companies.

Starting in the 1980s, Costa Rica abandoned the ISI model and embraced trade liberalization, creating an export platform based on attracting foreign investment in a tax-exempt regime, which helped it balance its public finances. The new model was able to take hold because Costa Rica's exports were protected by a system of preferences granted by the United States and the European Union, which had exempted Costa Rican exports from tariffs. However, these regimes were unilateral concessions with an expiration date, so when the time came for these preferential regimes to end, Costa Rica—like the rest of the Central American countries that had suffered the same fate—needed to negotiate free trade agreements with both the United States and the European Union. In those negotiations, which first took place with the United States, Costa Rican negotiators realized that they were required to eliminate state monopolies and fully open up communications and insurance companies to competition from international companies.

Costa Rica had to give in to preserve the new model of trade liberalization based on tariff concessions from the major importers of Costa Rican products. It was not an easy process, and to achieve it, a national referendum had to be held, the results of which showed a country deeply divided by the alternatives. However, both the opening up of communications and the opening up of insurance brought great benefits to consumers, who enjoyed better and more diversified access to both the insurance and telecommunications markets as a result of open competition.

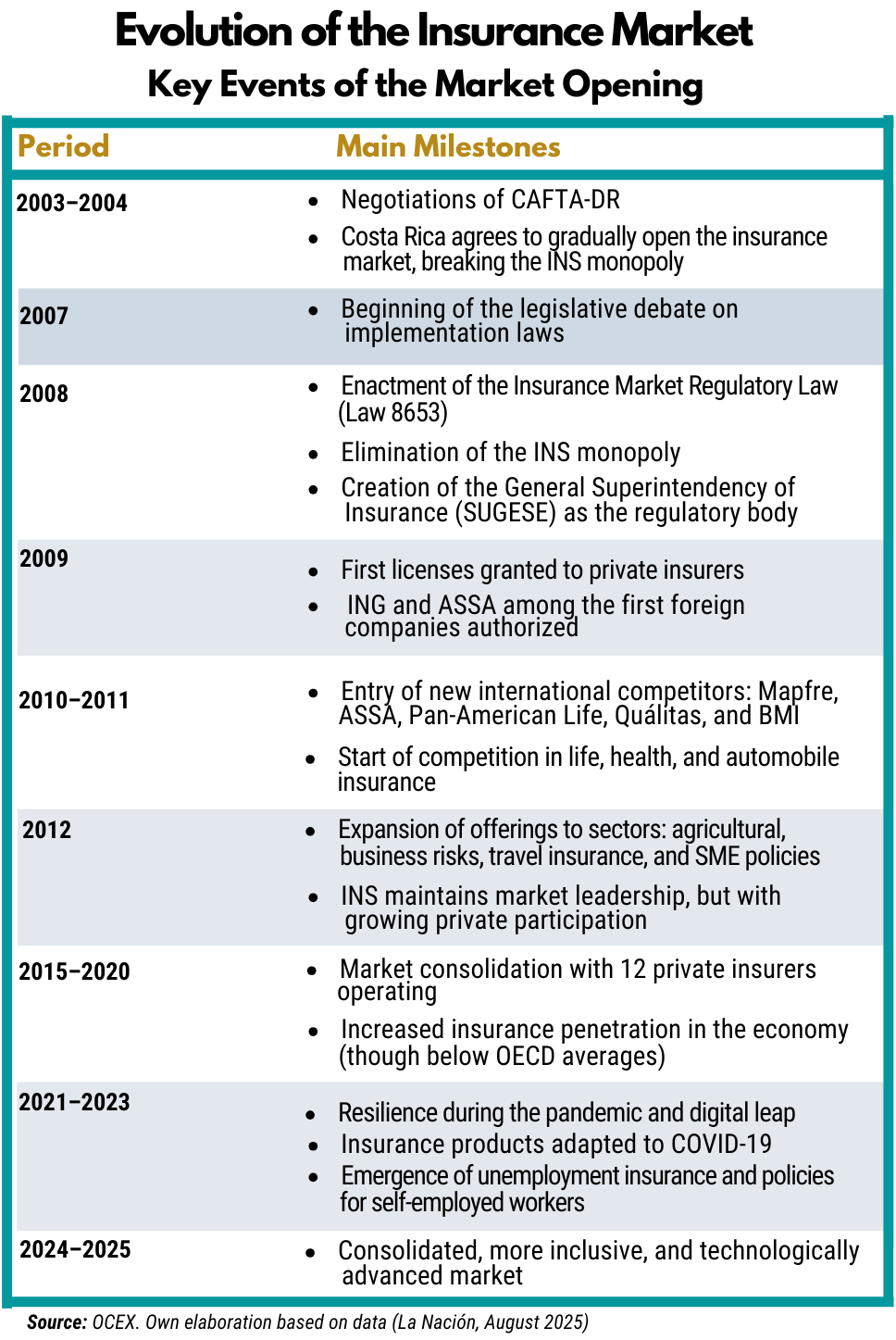

Key events that marked the opening of the insurance market. Broadly speaking, the process of opening up the insurance sector can be summarized as having been negotiated in 2003-2004, implemented with Law 8653 in 2008, and, subsequently, the entry of private competitors materialized in 2009, transforming the market. The table: Evolution of the Insurance Market details the main milestones.

In this Capsule N°5-2025, OCEX recounts the processes that took place in the insurance market.

Opening of the insurance market and CAFTA-DR. In 2008, Costa Rica underwent one of the most significant structural transformations in its economy: the opening of the insurance market. This decision not only ended a historic monopoly, but also laid the foundations for a more dynamic, competitive, and diverse sector. Seventeen years after this transformation, the country has consolidated a robust market with more players, more products, and a greater degree of financial inclusion.

Before the CAFTA-DR (Dominican Republic-Central America Free Trade Agreement) or TLC (Tratado de Libre Comercio entre República Dominicana, Centroamérica y Estados Unidos, in Spanish) came into force, the Costa Rican insurance market was closed to private competitors, both domestic and foreign. The National Insurance Institute (INS) held a legal monopoly on the provision of insurance services in Costa Rica. In the Financial Services Chapter of CAFTA-DR, Costa Rica committed to progressively liberalizing the insurance market. The opening was part of the market access concessions to bring to fruition what was agreed in CAFTA-DR.

CAFTA-DR has had a positive impact on member countries, increasing trade and investment. The entry into force of this trade agreement took place on different dates depending on the country concerned. El Salvador, Guatemala, Honduras, and Nicaragua in 2006; the Dominican Republic in 2007. In the case of Costa Rica, it entered into force on January 1, 2009, according to Law No. 8622 of November 21, 2007, published in Supplement No. 40 to Gazette No. 246 of December 21, 2007.

From monopoly to open market. In August 2008, the Costa Rican Insurance Market Regulatory Law (Law No. 8653) was passed after almost 84 years of state monopoly. This law created the General Superintendency of Insurance (SUGESE) as an autonomous authority and regulatory body attached to the National Council for Supervision of the Financia l System (CONASSIF), responsible for supervising the solvency, transparency, and stability of the market, establishing the legal framework for competition in the sector. This meant the end of the INS monopoly, but it also sought to modernize it for open competition and protected the rights of policyholders.

l System (CONASSIF), responsible for supervising the solvency, transparency, and stability of the market, establishing the legal framework for competition in the sector. This meant the end of the INS monopoly, but it also sought to modernize it for open competition and protected the rights of policyholders.

Summary of the main objectives of Law 8653. Consequently, it defined the guiding principles of a new open and regulated market, with financial soundness, technical regulation, new investment opportunities, and consumer protection, highlighting:

- Market opening. It ended the INS monopoly, allowing private and foreign insurance companies to participate in the Costa Rican market.

- Creation of the regulatory framework. It established the basis for the authorization, regulation, supervision, and operation of insurance activities, including brokerage and auxiliary services.

- Promotion of competition. It sought to create conditions for a more modern and competitive insurance market.

- Modernization of the INS. It promoted the modernization of the National Insurance Institute so that it could operate efficiently in an open market without losing its social role.

- Consumer protection. It ensured the protection of the rights of policyholders and third parties involved in the various stages of insurance contracts.

- Creation of SUGESE. It established the General Superintendency of Insurance as the body responsible for ensuring the stability and functioning of the market.

- Guaranteed financing for firefighters. It ensured the conditions for the Costa Rican Fire Department to receive adequate financing. The opening was gradual, beginning with personal insurance (life, health, accidents). It then expanded to general insurance, supplementary pensions, and reinsurance.

Role of SUGESE as a technical pillar. Over the course of 15 years, the General Superintendency of Insurance (SUGESE) has played a technical and strategic role. Not only has it issued regulations that define insurance conditions for the benefit of consumers, but it has also promoted a modern and sustainable vision of the insurance sector.

SUGESE has taken a proactive role in transforming the market. Since 2023, it has been part of a joint commitment by Costa Rica's financial superintendencies to integrate sustainability and climate resilience into the country's financial system. Through the “Superintendencies' Declaration on Climate Change,” commitments were established such as strengthening technical capacities, including climate variables in supervision, and promoting innovative financial instruments.

In May 2025, the Ministry of Finance and SUGESE presented a national assessment of financial protection gaps to the Global Shield initiative. This report revealed that 77.9% of the population and 80.1% of economic activity are located in areas at high risk from threats such as floods, hurricanes, or droughts. In addition, the report warned that if action was not taken in time, due to the increase in accidents, some areas could become “uninsurable.”

The strategy promoted by SUGESE not only proposes expanding coverage and making more flexible models, but also implementing insurance based on parametric indices (such as rainfall or temperature). In addition, the agency promotes good practices for climate change risk management through the issuance of guidelines.

Its key functions include:

- Ensuring the stability of the insurance system so that insurance products are available in all circumstances.

- Authorizing, regulating, and supervising insurance companies, reinsurers, insurance intermediaries, and other market participants.

- Educating consumers, promoting transparency, competition, and providing access to clear and timely information.

- Combating fraud and promoting innovation in the market.

In addition, SUGESE, as the guarantor of the system, promotes the use of new technologies to strengthen innovation in the sector. This, combined with the market's adaptation to the challenges posed by climate change, will allow the national economy to move forward in an environment of sustainability and digital innovation.

Positive impacts on the domestic market. The evolution of the Costa Rican insurance sector is an example of how market opening can become an engine of economic and social development when accompanied by strong institutions, technical regulation, and a focus on the consumer. A consolidated, more inclusive, and technologically advanced market has been achieved.

The sector faces many challenges, but the tests that the Costa Rican market has overcome have yielded favorable results, including a diverse offering with the addition of 12 authorized insurers, an expanding market with more than 2,000 registered intermediaries since its opening in 2008, and more than 700 authorized products. To date, the Costa Rican market has:

- 12 authorized insurers, including prestigious foreign companies.

- A diversified insurance offering, ranging from mental health policies to cyber risks.

- Greater public awareness of the importance of insurance to support financial security.

- Greater access to insurance for consumers and businesses.

- Improvements in efficiency and service, driven by competition.

- Modernization of the regulatory framework and institutional strengthening.

- Entry of private insurers: national and international (Mapfre, ASSA, Pan-American Life, among others).

- Competition in prices, coverage, and service quality.

- Product diversification: private health insurance, more competitive auto insurance, and niche policies (SMEs, agriculture, special risks).

- The INS lost its monopoly but retained its initial advantages based on its size and experience.

- Good practices in place: analysis of climate scenarios, identification of future risks, and projections. Implementation of preventive measures for early action to mitigate impacts. Strengthening of institutional capacities, improvement in management, coordination, and response, in accordance with the United Nations Development Program (UNDP) risk reduction and climate resilience programs.

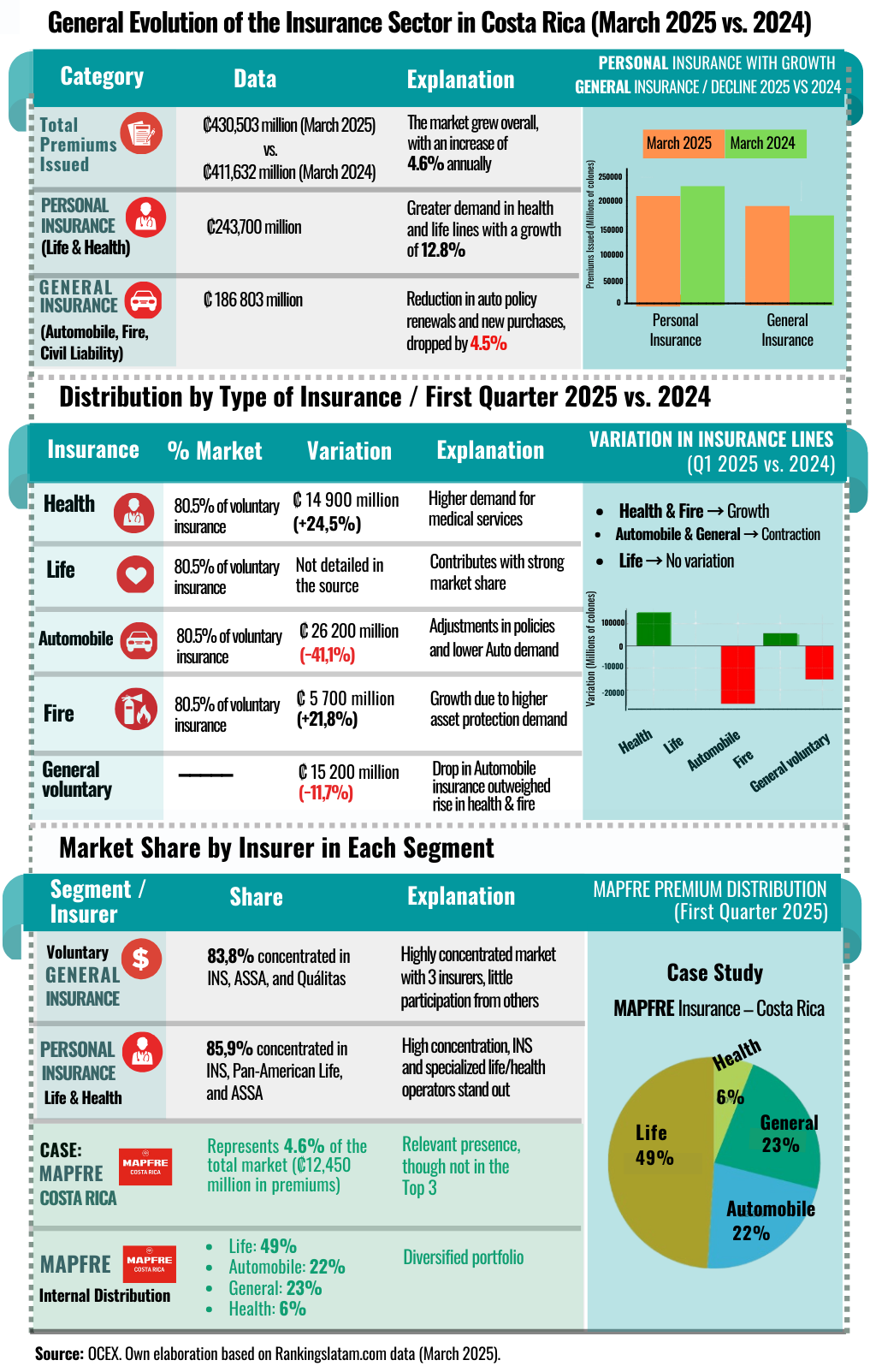

Overview of the insurance market. In the twelve months ending in March 2025, the Costa Rican insurance market showed moderate overall expansion, totaling 430.503 billion colones in premiums written, compared to 411.632 billion the previous year. Performance varied across segments: while personal insurance increased by 12.8%, reaching 243.7 billion colones, general insurance decreased by 4.5%, totaling 186.803 billion colones. Expressed in US dollars, market growth was more pronounced due to exchange rate fluctuations, rising from USD 832 million to USD 895 million, an increase of 7.6%.

Among product lines, the most significant contraction occurred in auto insurance, which fell 41.1% to 37.592 billion colones. This sharp decline contrasts with the solid performance of other segments, particularly health insurance, which grew by 24.5% to 75.887 billion colones, and fire and related insurance, which increased by 21.8% to 32.218 billion colones.

Compulsory automobile insurance (SOA) registered an increase of 9.6%, totaling 72.462 billion colones. This also reflects the growth of the country's vehicle fleet, as well as variations in vehicle prices. Compulsory occupational risk insurance (SRT) also grew by 9.6%, reaching 90.124 billion colones, which also reflects the growth of formal economic activity. Life insurance premiums stood at 70.194 billion colones, up 8.4% year-on-year.

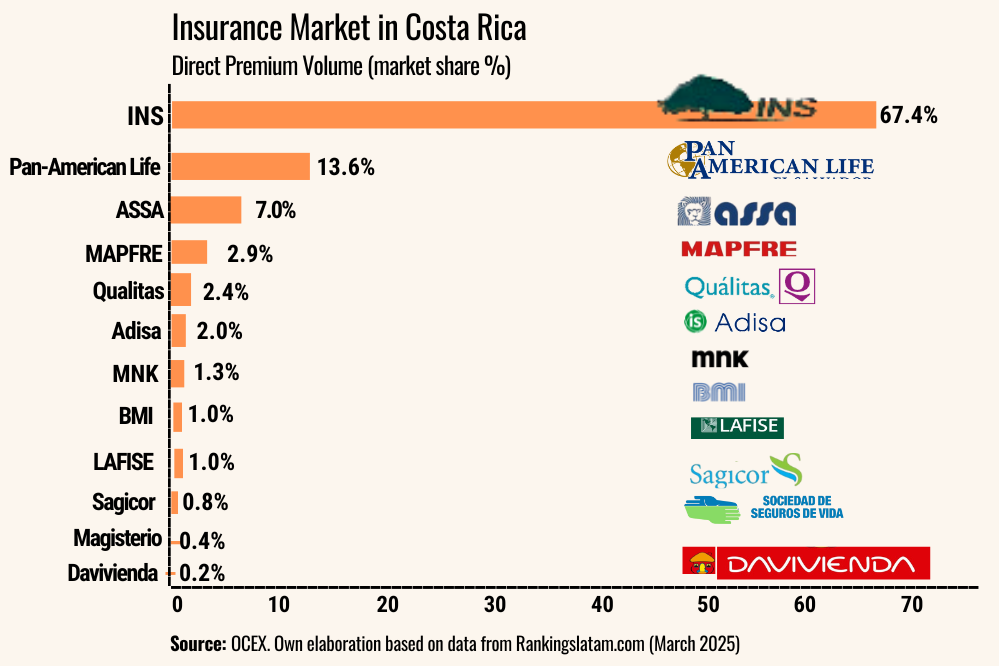

The INS maintained its market leadership, capturing 67.4% of total premiums, followed by Pan American Life with 13.6%, ASSA with 7.0%, MAPFRE with 2.9%, and QUALITAS with 2.4%. In terms of market share growth, Pan American Life recorded the most notable increase, with 2.14 percentage points. Other insurers that showed growth were MNK (formerly OCEANICA), with an increase of 0.43 percentage points, ASSA with 0.19, SAGICOR with 0.15, and LAFISE with 0.11.

Evolution of the insurance sector by segment and main insurance companies within each branch. Below is a broader and more detailed overview of the insurance market in Costa Rica, including data updated to the beginning of the third quarter of 2025:

- In general insurance, INS continue to be the main player, especially where its leadership is complemented by ASSA and Quálitas.

- In personal insurance (life and health), Pan-American Life stands out, along with INS and ASSA.

- Health and life insurance are the products with the greatest momentum in 2025, while auto insurance is experiencing a sharp decline in the voluntary market.

- MAPFRE has a solid position, with a diversified presence, especially in life and general insurance, although it is still far behind the three leading insurers.

Challenges for the insurance market. The tests that the Costa Rican market has passed have yielded a favorable balance that includes a varied offering with the addition of 12 authorized insurers, an expanding market with more than 2,000 registered intermediaries since its opening in 2008, and more than 700 authorized products. However, the following challenges remain to be overcome in the sector:

- Increase adaptation and mitigation of the impacts of climate change. The frequency and intensity of extreme events in Costa Rica (droughts, floods, storms) has increased. This affects infrastructure, crops, public health, and generates high economic and social costs. Sustainability, as a cross-cutting principle, requires us to think about products that respond to the need for new flexible and innovative schemes adapted to climate change.

- Implement insurance based on parametric indices. These are policies that do not provide compensation based on the actual loss suffered, but are automatically activated when a previously defined and measurable event occurs (an objective parameter: rainfall or temperatures).

- Strengthen social inclusion. The goal is to offer innovative channels and schemes adapted to different social and economic realities. We are facing a low level of insurance culture among the population, concentration in a few competitors, and a need to strengthen financial education. Therefore, products and models that reach more people, especially those who have historically been beyond the reach of traditional insurance, should be promoted.

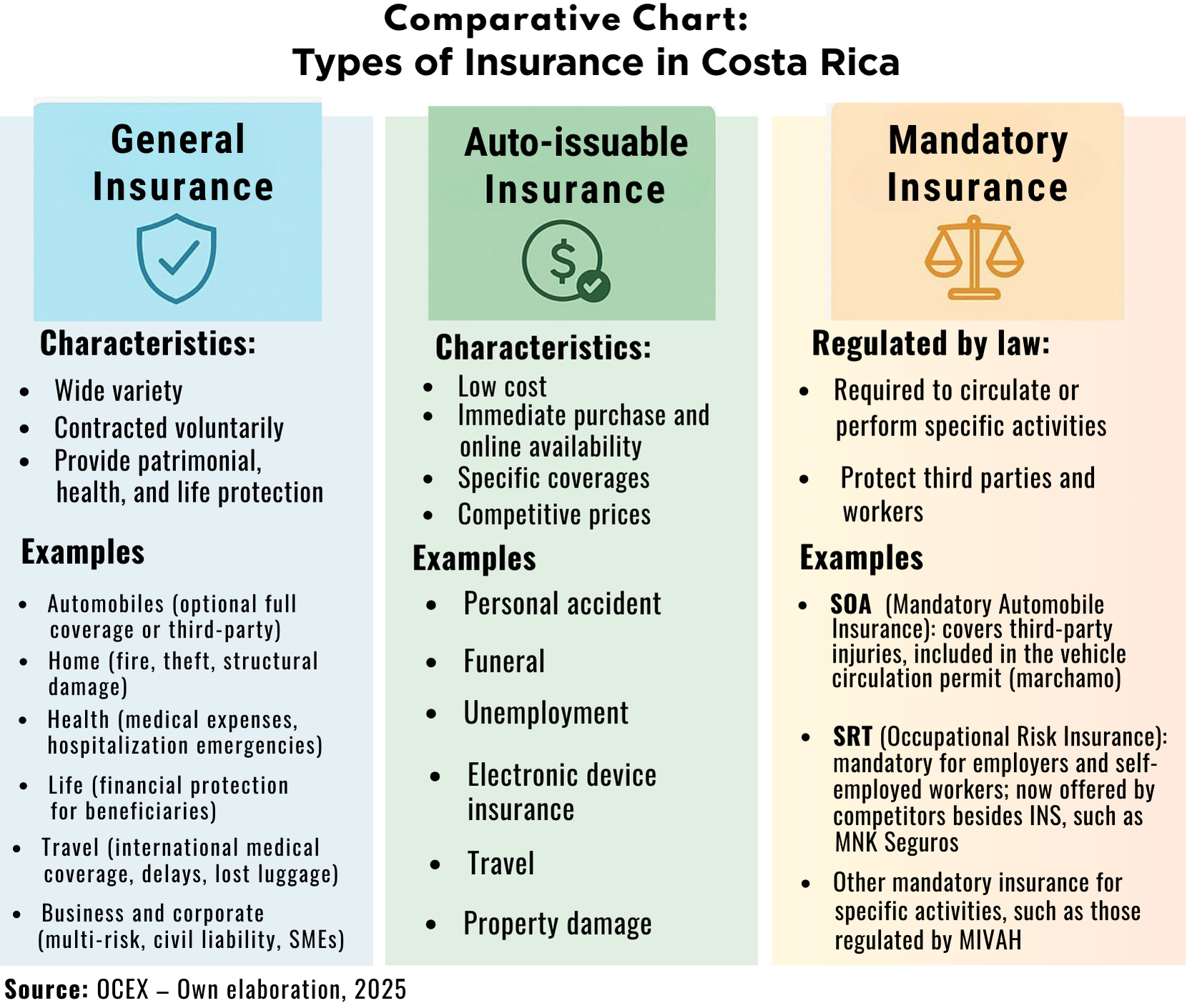

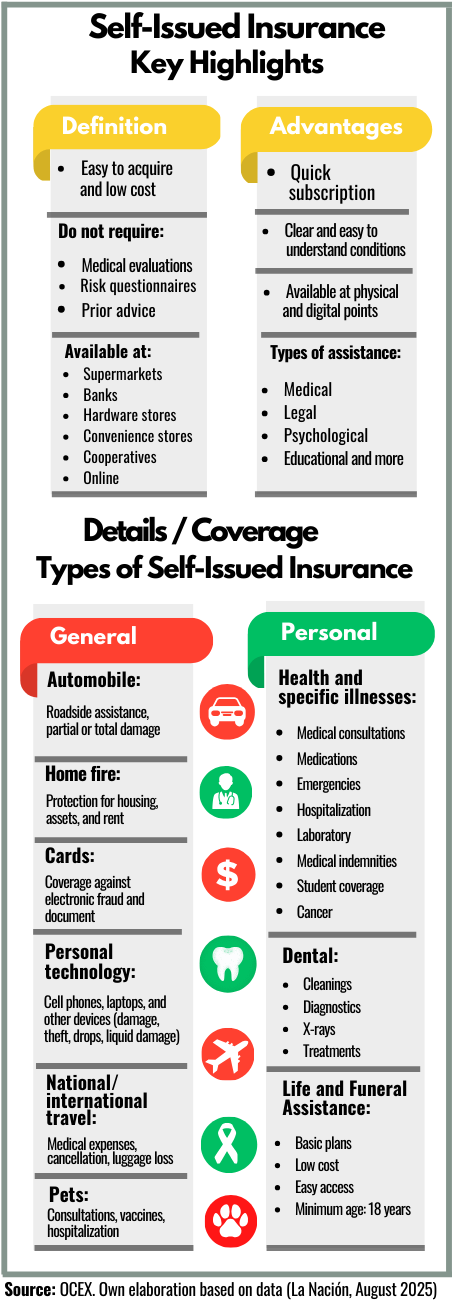

- Promote access to self-issued insurance. These are low-cost policies that are easy to purchase, either physically or digitally, at various types of commercial establishments. Currently, the market has 84 authorized operators, including commercial stores, hardware stores, grocery stores, and also banks, mutual societies, and cooperatives that are authorized to sell insurance from insurance companies.

- Promoting digitization is an important challenge, as it redefines the way insurance is designed, distributed, and supervised, opening up opportunities but also new requirements in terms of cybersecurity and consumer protection.

Lecturas consultadas:

- La República.net. La nueva generación de seguros. Mayo 2025. En: https://www.larepublica.net/noticia/la-nueva-generacion-de-seguros?utm_

- El confidencial.com. Presidente Arias firma ley de apertura del mercado de seguros en Costa Rica. Julio 2008. En: https://www.elconfidencial.com/mercados/2008-07-22/presidente-arias-firma-ley-de-apertura-del-mercado-de-seguros-en-costa-rica_1007861/?utm

- El Pais.com. Costa Rica revienta 84 años de monopolio estatal en seguros. Abril 2008. En: https://elpais.com/internacional/2008/04/26/actualidad/1209160801_850215.html?utm

- Revista Summa.com. Mapfre Costa Rica cierra primer trimestre 2025 con ₡12.450 millones en primas. En: https://revistasumma.com/mapfre-costa-rica-cierra-i-trimestre-2025-con-%E2%82%A112-450-millones-en-primas/?utm

- HR Insights. Mercado de seguros en Costa Rica presenta un crecimiento de casi 50% en 10 años. Mayo 2025. En: https://hr-insights.experienciawellbeingaon.com/noticias_externas/mercado-de-seguros-en-costa-rica-presenta-un-crecimiento-de-casi-50-en-10-anos-2/?utm

- The Global. El mercado de seguros en Costa Rica ya representa el 2,62% del Producto Interno Bruto. Julio 2024. En: https://theglobalcr.com/el-pais/mercado-de-seguros-en-costa-rica-presenta-un-crecimiento-de-casi-50-en-10-anos/?utm

- Delfino.cr. Mercado de seguros en Costa Rica casi duplicó su tamaño en la última década. Julio 2024. En: https://delfino.cr/2024/07/mercado-de-seguros?utm

- Ministerio de Comercio Exterior (COMEX). TLC entre República Dominicana, Centroamérica y Estados Unidos (CAFTA-DR). En: https://www.comex.go.cr/tratados/cafta-dr/

- Semanario Universidad. Participación del INS en primas de seguros paso de 72,45% a 70,99% en enero 2025. Marzo 2025. En: https://semanariouniversidad.com/pais/participacion-del-ins-en-primas-de-seguros-paso-de-7245-a-7099-en-enero-2025/?utm

- Rumboeconomico.net. Negocio de seguros en Costa Rica creció 5,5% en 2023. Octubre 2024. En: https://rumboeconomico.net/economia/negocio-de-seguros-en-costa-rica-crecio-55-en-2023/?utm

- Documentacion.fundacionmapfre.org. Mercado de Seguros de Costa Rica: Panorama y estadísticas del sector - Rankings a marzo 2025. En: https://documentacion.fundacionmapfre.org/documentacion/publico/es/bib/187940.do?utm

- La República.net. Mercado de seguros reporta crecimiento de 10% en colocación de primas para 2024. En: https://www.larepublica.net/noticia/mercado-de-seguros-reporta-crecimiento-de-10-en-colocacion-de-primas-para-2024?utm

- El Financierocr.com. Los seguros son una herramienta de adaptación ante el cambio climático. En:https://www.elfinancierocr.com/gnfactory/brandvoice/2021/sugese-webinar-cambio-climatico/index.html?utm_

- Bilaterals.org. Costa Rica rompe monopolio de seguros tras 84 años. Fin del monopolio estatal del INS después de décadas. Abril 2008. En: https://www.bilaterals.org/?costa-rica-rompe-monopolio-de

- La República.net. Monopolio del INS llega a su fin. Sanción de la ley que abre el mercado (Ley 8653). Julio 2008. En: https://www.larepublica.net/noticia/monopolio-del-ins-llega-a-su-fin

- Panamá. La Prensa.com. Costa Rica lista para abrir mercado de seguros. Entrada de aseguradoras privadas al mercado costarricense. Diciembre 2009. En: https://www.prensa.com/economia/Costa-Rica-lista-mercado-seguros_0_2731227074.html#google_vignette

- BLP Legal (blog). A 10 años de la apertura del mercado de seguros. Retrospectiva y vínculo con el referéndum del CAFTA-DR y sus efectos en el sector. Agosto 2019. En: https://blplegal.com/es/a-10-anos-de-la-apertura-del-mercado-de-seguros/

- El Financiero CR. A 10 años de la apertura del mercado de seguros. Evolución regulatoria y vínculo con el TLC y la Ley 8653. Agosto 2018. En: https://www.elfinancierocr.com/opinion/a-10-anos-de-la-apertura-del-mercado-de-seguros/PAZRVF7BKZFF7KNYB3IGQOBFG4/story/

- Boletines.latinoinsurance.com. Mercado de seguros cerró con un crecimiento del 4,5 % en el primer trimestre del año. Junio 2020. En:https://www.crhoy.com/mercado-de-seguros-cerro-con-un-crecimiento-del-45-en-el/

- Newsletter Rankingslatam.com. Mercado de Seguros de Costa Rica: panorama y estadísticas del sector. Rankings a marzo 2025. En: https://rankingslatam.com/es-la/blogs/industry-news/costa-rica-insurance-market-industry-overview-and-statistics-march-2025-rankings

- La Nación. SUGESE: evolución, inclusión y futuro del mercado asegurador costarricense. Agosto 2025. En: https://www.nacion.com/brandvoice/contenido-a-la-medida/sugese-evolucion-inclusion-y-futuro-del-mercado/DVLQQS2Z5RBJJAIJMVX7XQDM3M/story/